#Financial Literacy #SEP

CPF Basics for Arts SEPs

3 April 2025

A guide to understanding CPF contributions for arts Self-Employed Persons

Why CPF Matters for Arts SEPs

As a self-employed arts professional, managing your CPF contributions is crucial for:

Future housing loans and credit applications

Healthcare coverage

Retirement planning

How CPF works

The Central Provident Fund (CPF) is a key pillar of Singapore’s social security system. CPF helps Singapore Citizens and Permanent Residents set aside funds to build a strong foundation for retirement.

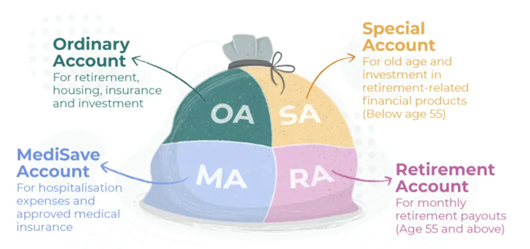

Your CPF accounts

If you’re self-employed, you need to contribute to MediSave. These savings will be especially important in old age when you may have stopped working.

🥇 Understanding MediSave Requirements

Mandatory for SEPs earning annual Net Trade Income (NTI) above $6,000

Helps secure healthcare needs, especially for retirement

Contributions based on your Net Trade Income (NTI)

CAYE Scheme: What You Need to Know

The Contribute As You Earn (CAYE) scheme helps self-employed persons (SEPs) contribute to their MediSave as and when they receive service payments.

Key Features:

Automatic MediSave deductions from government service payments

Contribution rate varies based on:

Your age

Estimated Net Trade Income

CAYE contribution rate

How it Works:

Government agencies deduct MediSave contribution from your service fee

Amount transferred directly to your MediSave account

Helps build healthcare savings through regular small contributions

🥉Voluntary CPF Contributions

Beyond MediSave, you could earn 4% interest by contributing a sum to your CPF Special Account, for instance.

Optional contributions to Ordinary and Special/Retirement Accounts

Benefits of voluntary contributions:

Enhanced retirement savings

Potential tax relief

Higher interest rates compared to bank savings

Next Steps

Check your annual NTI to determine MediSave obligations

Understand CAYE deductions for government projects

Consider voluntary contributions based on your financial goals

Useful Resources